Understanding Derivatives

Derivatives, or futures contracts, are a type of financial instrument created to allow a buyer and a seller to enter into an agreement to trade — or grant the right to trade — an underlying asset in the future. These contracts clearly specify the type of asset, specifications, price, quantity, settlement method, and expiration or delivery date.

In derivative trading, The buyer is said to hold a "Long" position,While the seller holds a "Short" position.Therefore, a derivative or futures contract does not have intrinsic value on its own. Its value is derived from the price of the underlying asset it is based on.

Types of Derivatives

In financial markets, derivatives are typically divided into four categories:

Futures, Options, Forwards, and Swaps.

In Thailand’s derivatives market (TFEX), only two types are actively traded:

Futures

A futures contract is an agreement between a buyer and a seller to buy or sell an underlying asset at a specified future date, with the terms of the trade — including the asset type, specifications, price, quantity, settlement method, and expiration date — agreed upon today.

Options

An option contract gives the buyer the right, but not the obligation, to either: Buy the underlying asset (Call Option), orSell the underlying asset (Put Option)

from the seller, at a predetermined price and quantity, within a specified period. The contract includes an expiration date. The seller is obligated to fulfill the contract terms if the buyer exercises the option, while the buyer has the right to choose whether or not to exercise that option.

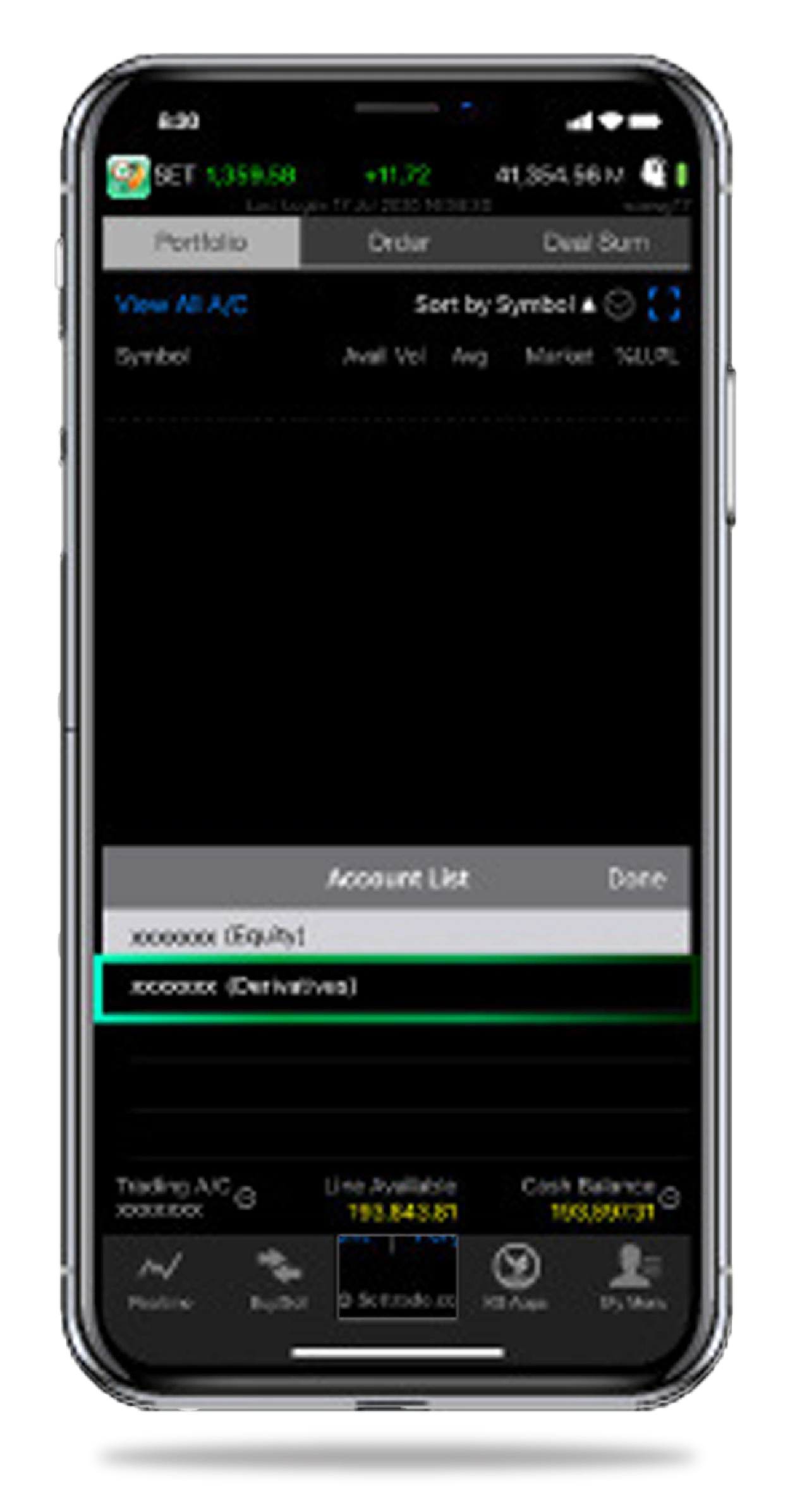

Early Exit Before Expiration

Both Futures and Options do not require investors to hold the contract until expiration.

Investors may close their positions or exit the contract at any time through trading on the TFEX (Thailand Futures Exchange).

ภาษาไทย

ภาษาไทย

English

English

)

)

1 1.png)

1.png)